Options, Edge, and Risk - A Clear-Eyed View

One of the most common misconceptions I encounter is that options are inherently more risky than stocks. This belief, while widespread, demonstrates a fundamental misunderstanding of both investment vehicles. The truth, as is often the case in investing, is more nuanced.

The Nature of Edge

Let's start with what really matters: edge. Edge isn't about the instrument you're trading – it's about the probability-weighted outcomes of your investment decisions. When you have edge, you have a situation where the expected value of your investment is positive. This is true whether you're trading stocks or options.

Consider a simple example: You identify a stock trading at $50 that you believe has an 80% chance of being worth $75 and a 20% chance of being worth $25. Your expected value is:

- (0.80 × $75) + (0.20 × $25) = $65

This gives you $15 of edge ($65 - $50). The presence of this edge is what matters, not whether you express it through stocks or options.

The Options Advantage

In fact, there are scenarios where options can actually reduce risk. With certain option strategies, you can create positions where your maximum loss is known and limited, while still maintaining exposure to your edge.

The key is in the sizing.

Options Can Give You Leverage

If you have $100,000 to invest and strong conviction in a stock, you might invest $25,000 directly in shares. But what if you could leverage that bet while taking less exposure using options for $5,000 in premium? You've maintained your upside while reducing your capital at risk.

Risk and Reward - A Framework

The decision between stocks and options should be based on:

- The clarity of your catalyst

- The volatility environment

- Your ability to quantify edge.

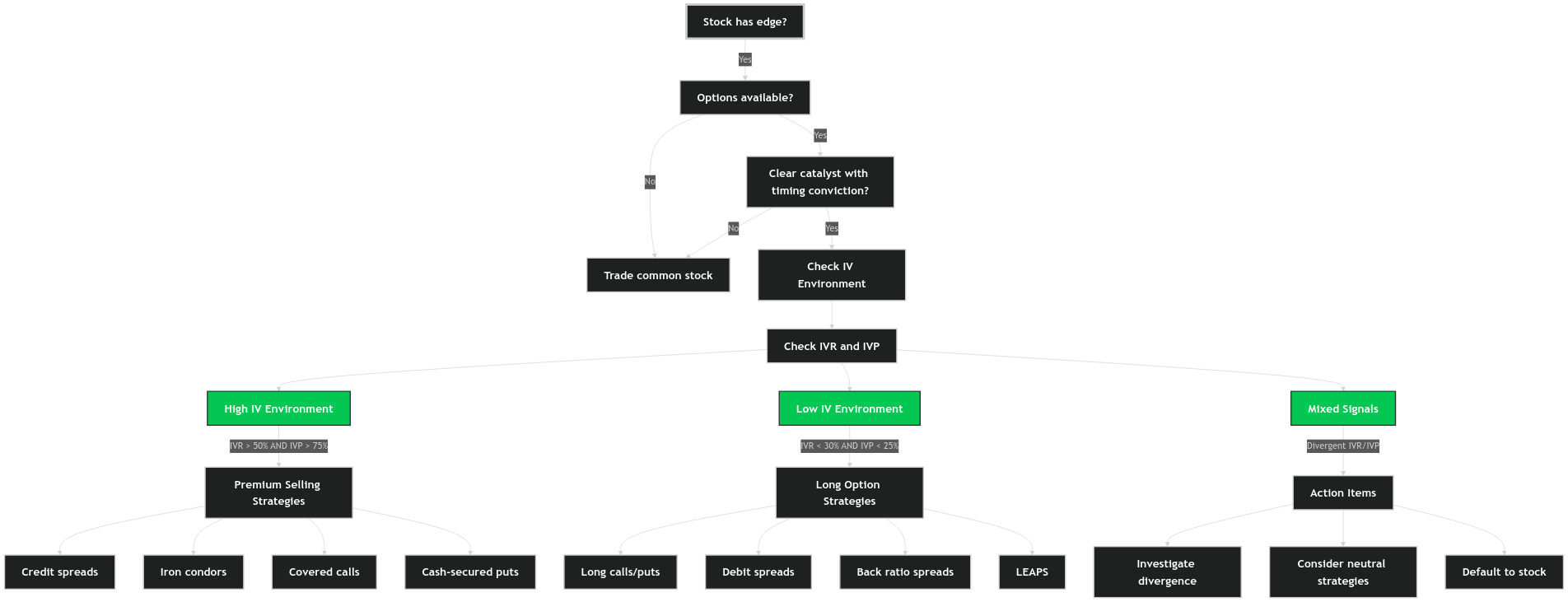

Volatility Environment

IV Rank and IV Percentile help us determine if current implied volatility is relatively expensive or cheap compared to the stock's own history. Let me break down how to use each:

IV Rank:

Measures where current IV is relative to its 52-week high/low range Formula: (Current IV - 52-week Low) / (52-week High - 52-week Low) × 100

Example: If IV is:

-

52-week High = 60

-

52-week Low = 20

-

Current IV = 28

-

IV Rank = (28-20)/(60-20) × 100 = 20%

-

Under 25-30 = Low

-

Over 50-60 = High

IV Percentile:

- Percentage of days over past year IV was lower than current IV

- More granular than IV Rank

- Example: If current IV is higher than 80% of the past year's readings, IV Percentile = 80

Quick Volatility Guide

HIGH IV (expensive options) ->

- Need to consider if the catalyst timing justifies paying high premium

- Might want to consider selling premium instead

- Need to compare to historical volatility (HV) to see if overpriced

LOW IV (cheap options) ->

- Long options strategies become more attractive

- Less premium at risk

- Better risk/reward for directional bets

The Real Risk

The greatest risk in options isn't the instruments themselves – it's not having a systematic framework for making decisions. This is why we use decision trees and strict criteria for evaluating opportunities. Without these, you're not investing – you're speculating.

Looking Forward

As we navigate 2025's markets, I'm finding opportunities in both stocks and options. The key isn't to categorically prefer one over the other, but to:

- Identify genuine edge

- Quantify the edge precisely

- Choose the most efficient instrument to express that edge

- Size the position appropriately

Remember: Risk doesn't come from what you're trading. Risk comes from not knowing what you're doing.

The Bottom Line

Options are tools – nothing more, nothing less. In the hands of an investor who understands edge and position sizing, they can actually reduce portfolio risk while maintaining upside exposure. The key is having a systematic framework for making these decisions.

As always, the goal isn't to avoid risk – it's to understand it, quantify it, and get paid appropriately for taking it.

Best regards, Tyler DuPont

P.S. - Want to better manage your portfolio using Augury?